WHY GOVERNMENT SHOULD SELL EVEN PROFIT-MAKING STATE-OWNED ENTERPRISES

Posted on April 30th, 2023

By Sanjeewa Jayaweera Courtesy The Island

The recent pronouncement by President Ranil Wickremesinghe (RW), that The government has no business to be in business.” was music to the ears of those who believe in a free market economy. However, it also drew the ire of the loony left, the trade unions, a few die-hard academics who still cling to ideals of socialism as well as a few journalists.

In all probability, if a straw poll is conducted, most voters would say that the Government of Sri Lanka (GOSL) should continue to own and operate state-owned enterprises (SOEs). It is indeed a paradox that despite it being well-known that SOEs are inefficient, corrupt and a drain on taxpayer funds due to significant losses, many in our country still believe privatization is undesirable. One can only assume this is due to the entitlement mentality ingrained in us over several decades and the belief that the government should be our provider.

What ails the SOEs

Citizens ultimately own SOEs but have no voice and lack the interest or wherewithal to monitor them. Therefore, efficiency is entirely dependent on the existing system of governance. Political patronage is the criterion for selecting the top management of SOEs allowing government politicians to choose their relatives and close friends despite their having no prior experience in holding such positions. That such appointments have resulted in adverse consequences to the enterprise and the country is a well known fact.

Employment in state institutions has been on a ‘Jobs for the Boys’ philosophy to which many, including university graduates, subscribe. All SOEs are overstaffed primarily due to elected politicians using their power and influence to overload them despite no existing vacancies. The problem has been compounded by the fact that most of those appointed are poorly skilled. Once employed, they join trade unions and demand above-average wages and bonuses even when losses are being incurred. They want their personal income tax paid by the SOE and light work norms. So it is not surprising that despite the economic Armageddon we have hit, many still hang on to the belief that the government should be running businesses.

The need to educate the public

The recent announcement by the government that it intends to divest its investments in Sri Lanka Telecom (SLT), Lanka Hospitals (LH), and the Sri Lanka Insurance Corporation (SLIC) has resulted in many, including the leader of the opposition, the JVP, trade unions, a few journalists and other media personnel together with some academics to say We are against the privatization of profit-making SOEs.” Their opposition to the sale resonates with the public and supports the theory of selling the family silver.

When a young journalist posed this question to RW at a media conference, he told her in his typically offhand and condescending tone, We have debts to settle as well.” I believe it was an opportunity lost by RW to explain through the media to the people why it makes perfect sense to dispose of the shares held in SLT, SLIC and LH.

In my opinion, when it comes to the economy and finance, most people in our country are ignorant. Many highly educated people and experts in their own field I know say, I don’t know or understand finance.” In the last couple of years, we have seen greater discussion and information sharing on the economy and finance due to the economic crisis. However, there is still a lack of understanding and proper appreciation of the issues. The government must disseminate the policy through its media with greater focus and transparency. I have often been dismayed when RW and other government officials say, The IMF has told us to do this and that”. Instead of passing the buck to the IMF, GOSL needs to say commonsense and financial prudence demands what we’re doing.

Why it’s sensible for GOSL

to sell its SLT stake

For me, the logic in selling the shares of profitable enterprises is evident on both financial and ideological grounds. In the case of SLT, the GOSL, through the Treasury and the Employees Trust Fund (ETF), currently own a controlling 50.9% of the company. A share of SLT trades presently at around Rs. 94 on the Colombo Stock Exchange. This means the company’s value is around Rs. 168 billion. Therefore the GOSL stake is worth around Rs. 86 billion.

However, the current market price of an SLT share is significantly overvalued due to the anticipated sale of the government stake. According to the company’s latest Annual Report, in the last 10 years up to the end of 2021, the highest price the share commanded was Rs. 57.30 in 2014. However, in 2022 the highest traded price was Rs. 78.90, whilst the lowest was Rs. 28.70. Obviously, an independent valuation would need to be carried out considering that a controlling stake is being sold. Several well-established methodologies are used in the valuation of companies.

To illustrate my point that it is beneficial for GOSL to sell out, I will assume Rs. 65 per share is the price the government will get on the deal. The GOSL would therefore be able to receive Rs. 59.7 billion by selling its SLT stake.

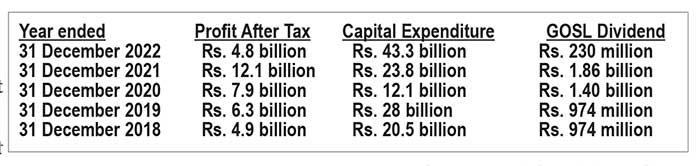

I have set out below the last five-year financial performance, capital expenditure and dividends paid to GOSL by the SLT Group.As can be observed, despite posting healthy profits, the dividends declared have been constrained by the high capital expenditure incurred. Given the rapid technological development and the ever-expanding use of mobile communication and the Internet, all telecommunication companies need to incur continuous capital expenditure to keep abreast.

The table shows the GOSL has only received total dividends of Rs 5.4 billion over five years, an annual average of Rs 1.1 billion a year.

So the question is whether retaining its SLT shares and earning Rs. 1 billion a year against receiving Rs. 59.7 billion as sales proceeds, is beneficial to the country or not. As stated by RW , the GOSL by selling could then utilize the Rs. 59.7 billion proceeds to retire some of its current debt and also not raise new loans as is currently done at interest rates above 20% plus. The interest saving for a year on the new debt at 20% would be Rs. 12 billion.

Opportunity cost is the criterion for making prudent financial decisions. The definition of opportunity costs is the value or benefit of what you lose or miss when you choose one alternative over another. In this instance, in case the GOSL does not sell its SLT stake at my assumed price of Rs. 65 per share, the opportunity cost foregone is Rs. 11 billion for a year.

The sale of SLT shares will not impact on our national security as the largest telecommunications operator in the country is a foreign-owned entity.

In 1997, the government, through a competitive bidding process, sold 35% of its shareholding in SLT to Nippon Telegraph and Telephone (NTT) of Japan for US$ 225 million. This was then the largest ever privatization transaction of GOSL.

The transformation of SLT under a Japanese CEO after partial privatization was immense and is often cited as an example of why SOEs should be privatized. The days when we had to wait nearly five years to get a new fixed-line connection were ended as SLT was transformed into a service-centric business enterprise. However, even after two decades, the Chairman of SLT, in his message to the shareholders in the 2021 Annual Report, laments, In January 2020, we saw a company with immense potential, but its progress was obstructed in several areas. Staff unrest was at the top of the list with regular strikes and work stoppages leading to poor messaging (signalling) to the customers, especially the corporate sector.”

Staff remuneration cost at SLT versus its competitor

According to the latest Annual Report (AR), SLT employed 8,058 staff. In 2021 costing Rs. 20.7bn. wages. In contrast, Dialog Axiata Plc, its main competitor, with a significant market share (17.7 mn subscribers vs SLT’s 9.3 million) and revenue (Rs 142 Bn vs Rs. 102Bn) over SLT, employed only 3,631 staff with a total wage bill of Rs. 10 bn. The bottom line is that SLT incurs Rs. 10.7 bn staff costs over its competitor to service a subscriber base significantly lower than its rival. These figures reflect the cost inefficiencies at SLT and other SOEs and is the primary reason the trade unions vehemently oppose the sale of the GOSL stake.

Furthermore, Dialog Axiata Plc has stated in its Annual Report that they have invested US $ 3 Bn since inception. In 2021, they paid Rs 8.4 billion as direct taxes and collected Rs. 14.8 Billion as consumption taxes. Another benefit of privatization for the GOSL is that it stands to collect higher direct taxes from companies operating efficiently with a cost focus.

The logic I have applied to the sale of the SLT stake is equally applicable to the sale of the GOSL stakes in Lanka Hospitals and Sri Lanka Insurance Corporation.

We need to set aside, at least now, this long-held view that the government should be involved in controlling and operating businesses. The process of privatization is lengthy and, as can be seen, will meet various hurdles. However, the GOSL must be steadfast in its determination to go ahead with the planned privatization/restructuring process of SOEs and actively engage the public and educate them of the benefits.

Transparency and competitive bidding when Privatising SOEs

A mandatory requirement for privatization is that the process must be totally transparent and be based on competitive bidding. Furthermore, the base price/valuation for sale should be arrived at by an independent party so that they are no doubts that the GOSL and the people received the best possible deal.

The success of India

Sri Lanka should look across the ocean at India, which since 1991 has been following a strategy of Liberalization, Privatization and Globalization that has led to consistent economic growth; India is now considered a global economic powerhouse. A few years back, Prime Minister Narendra Modi said the government has no business to be in business, and his administration is committed to privatizing all PSUs barring the bare minimum, in four strategic sectors.

It is the government’s duty to support enterprises and businesses. But it is not essential that it should own and run enterprises,” he said. Modi also said the Centre’s policy is to either monetize or modernize public sector enterprises on the basis that the government has no business to be in business”.

(The views and opinions expressed in this article are of the author and are not of any institution or organization that he may be associated with.)